A fire broke out at the Habshan gas processing complex in Abu Dhabi after debris from intercepted ballistic missiles fell on the site during an attack on the United Arab Emirates, AzerNEWS reports.

Day: April 3, 2026

Growing tensions around the Strait of Hormuz are raising concerns about global energy security and accelerating the search for diversified supply routes. In this context, Azerbaijan is strengthening its position as a reliable energy partner, expanding gas supplies to Europe and reinforcing its strategic role in the evolving energy landscape.

Why Armenian journalists are leaving the profession

In recent years, a clear trend has emerged in Armenia: experienced journalists with long careers are choosing to leave the profession. Why is this happening? We asked them directly.

Some have already found themselves in new careers, while others are still searching. Here are the stories of three former journalists.

- ‘There are no taboo topics’: Expert analyzes the media situation in Armenia

- 56 cases of media restrictions in Armenia: a three-month review

- 29 lawsuits against media in Armenia in six months

From journalism to cooking

Anna Satyam is a journalist with 23 years of experience. She left the profession and now dreams of opening her own small restaurant — something unique, unlike others.

“Journalism is not just a job, it is a way of life. You live in a reality where your life and work merge into one. The profession has a rhythm that becomes addictive. It has a dynamic that makes you feel useless without it. But after years, you suddenly realise you no longer want to write and start dreaming about something else,” she says.

Anna Satyan spent 11 years as deputy editor-in-chief of the newspaper Novoye Vremya. She then edited the Style section at news.am for five years. At the same time, she taught at the Faculty of Journalism at the Russian-Armenian (Slavonic) University. She decided to leave the profession while editing yet another article.

“Working with letters and words started to make me feel unwell. I thought maybe I was just tired, that I would go on holiday, rest, and it would pass. But it didn’t. I wrote about politics, the economy, everything. I worked 24/7. I had to stay available at any time of day, anywhere in the world. One day, I realised I didn’t want to live at that pace,” Anna says.

She lists several reasons that, together, pushed her to resign:

“After the 2020 war, something broke inside me. Then I had a severe case of коронавирус. It was a difficult, depressive period. To be honest, I felt uneasy in that reality. I lost the sense of comfort and harmony. I also no longer had people I wanted to work with. I began to see my work as meaningless.

I still don’t see myself in that reality. It’s sad, but true. I see a decline in intellectual standards around me. I don’t want to sound like a snob, but I went to press conferences and felt struck by the lack of clear thinking. And finally, I simply did not want to write anymore. I didn’t even want to turn on my computer.”

In 2023, she enrolled at the Yeremyan Projects Academy of Culinary Arts and Hospitality. She believes that running a restaurant requires a deep understanding of how a kitchen works.

“I enjoyed studying for six months. Then I completed a one-month internship and passed my exams. We studied cooking techniques and chemical processes. Cooking is chemistry. Sometimes we spent the whole day cutting carrots. For example, one hour cutting them large, another into thin strips, until our hands learned the movements and they became automatic. When I cut carrots, I felt relaxed. My thoughts were no longer like they were in journalism. I liked that,” Anna says.

The idea of opening a restaurant is still at an early stage, but she has already developed a business plan and menu:

“Even a small place like the one I imagine requires serious investment. People say the menu I created is very strong. They suggest I sell it and offer large sums of money. But no, I keep it for myself. I could take a bank loan or invest everything I have, but the risks are high. I feel an inner hesitation. I see how restaurants open and close. Some people take that risk easily. They think: if it works, great; if not, so be it. But I can’t think that way. I need to build a team and plan everything down to the smallest detail.”

For now, Anna runs a blog on a wide range of topics, sharing content on cooking, music and perfumery:

“Will this bring me back to journalism? I don’t know, I’m still figuring things out. I’ve accumulated so much — knowledge about music, perfumery, cuisine. I listen to different podcasts. I’ve immersed myself in all of this and want to share my new experience. It feels like I’ve gathered all my potential into a box that I want to share, and I’m sitting with it, thinking.”

She admits she still does not know where she wants to work:

“I probably no longer want to work for someone else. I want to have my own business, but I’m still in a state of uncertainty. At the same time, I need self-expression, which is why I started the blog.”

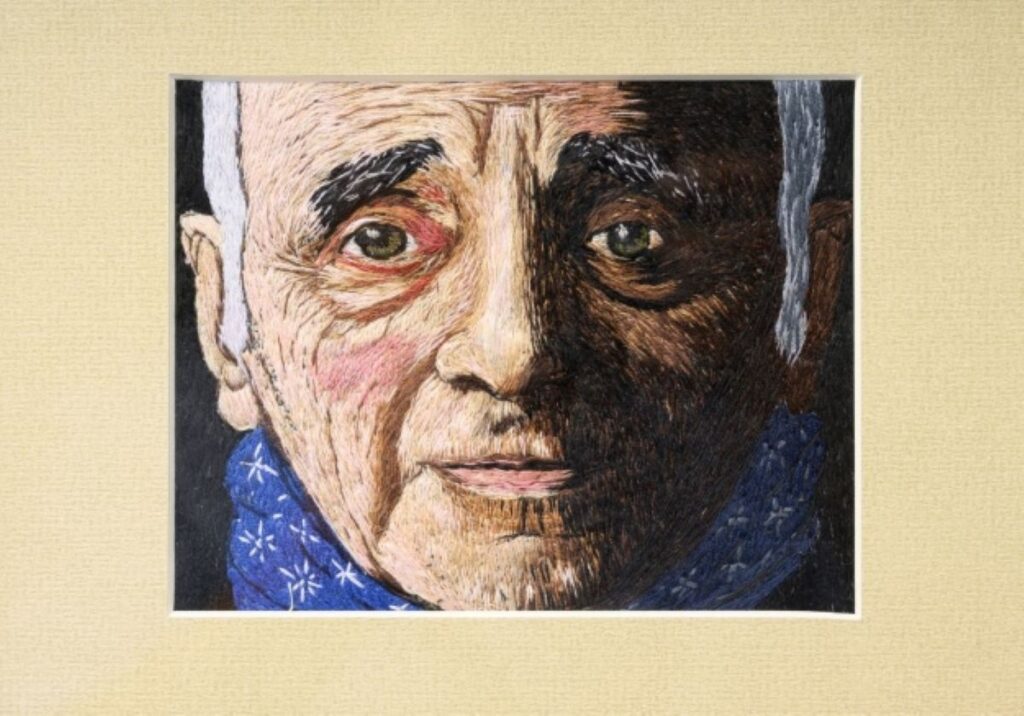

From journalism to embroidery

Journalist Kristine Khanumyan has started creating embroidered artworks and unique, hand-embroidered bags. Her grandmother and mother practised embroidery, but she never saw herself following that path.

“My grandmother was a weaver and worked at a silk factory, while my mother was a professional fashion designer. I grew up surrounded by threads, needles and fabrics. I found myself immersed in that world from childhood. But I always believed it was not for me, that I did not have enough patience.

I worked as a journalist for many years, but at some point I felt it was over. This began during the blockade of Artsakh. I understood in advance where things were heading, yet deep down I still hoped for something. Then I saw that nothing was happening, and my instincts proved right. I saw not only the end of my homeland, but also the end of my journalistic path. So I turned to embroidery,” she says.

The journalist worked in the former, unrecognised Nagorno-Karabakh Republic, writing for the newspapers Azat Artsakh (Free Artsakh) and Demo. From 2005, she contributed to Armenian outlets including Haykakan Zhamanak (Armenian Time), Zhamanak (Time), Chorrord Ishkhanutyun (Fourth Power), and from 2012 to 2023 to the website iLur.am.

She says journalism always held deep importance for her.

In 2012, when she began covering negotiations on the Karabakh conflict, she felt a heightened sense of responsibility. She was now reporting on the very question of whether her homeland would continue to exist.

She says two main reasons led her to leave the profession:

“In 2023, my narrow specialisation effectively disappeared. [In September 2023, a decree ended the existence of the NKR.] I could only explain why things had turned out this way. The second reason is that the media landscape changed. Media outlets turned into defenders either of the current government or of the former authorities. I no longer see neutral journalism. For me, journalism cannot be propaganda. That is why I decided to leave.”

She does not regret leaving the profession and has no intention of returning. She says she may one day write about how the negotiation process unfolded:

“But that text will have nothing to do with journalism, especially modern journalism. My current work demands far greater intellectual effort and creative thinking. I needed to do something fundamentally different — something artistically meaningful. I grew up in this environment and saw how beautiful work is created. I made this decision in a single day. I realised I did not need to look far or reinvent the wheel. I simply needed to return to my roots.”

From journalism to tourism and grooming

Journalist, marketing and social media specialist Eleonora Araratyan gradually realised that life was changing and pulling her away from the work she once loved:

“It became difficult for me to go to interviews. I would spend days working on a single piece. That made me realise I no longer wanted to write. I didn’t want to open my computer, read or write articles and press releases. I understood that I could no longer do this.”

After graduating from the Russian-Armenian (Slavonic) University in Yerevan, Eleonora went to Moscow to study at the Higher School of Economics. She later worked at the ARKA news agency and for the outlets Tert.am and Mediamax.

“My development as a journalist took place at Mediamax. I always saw journalism as a social responsibility — a way to solve problems. But after 2014, that role started to lose its value. Problems stopped being resolved. Journalists had once enjoyed respect, but something changed during that period. Funding departments in newsrooms began to grow. Advertising, banners and press releases became more important, while original reporting moved into the background. That suffocated journalism,” she says.

After the 2018 “Velvet Revolution”, she believes many people in Armenia began to see themselves as journalists and bloggers:

“Social media turned into a platform where anyone can speak out. Everyone started to see themselves as specialists or experts, and to treat their opinions as valid and important. I realised that both of my professions were losing value, and I could lose my job at any moment. I think you always need a plan B and additional skills. In this world, at this stage of life, when you are no longer young, you have to think about the future,” says the 42-year-old former journalist.

After returning from Moscow, she began hosting visitors from Russia from time to time, showing them around Armenia and introducing them to its landmarks.

“At first, it was a hobby. But I have now completed courses and qualified as a guide. I work with Russian tourists and organise hiking trips. I am also a member of the Armenian Mountaineering Federation. I enjoy interacting with people. It’s a very active and dynamic job,” she says.

During the COVID-19 pandemic, Eleonora got a dog, which eventually led her to pursue another profession:

“Since last year, I have been working as a groomer. Tourism and grooming are seasonal for me. I want to open my own grooming salon. I won a grant in a competition for women entrepreneurs, so I may soon be able to start my own business.”

Eleonora says her outlook on life and her role has changed over time:

“I now prefer physical work and like to see tangible results. Once someone told me: ‘You have two higher education degrees, and now you cut dogs’ hair?’ It upset me. I respect any kind of work, but those words still hurt. I wondered if I had made a mistake by leaving a profession I had worked in for so many years. But my friends told me I am simply versatile and capable of achieving anything. That comforted me. Journalism, PR and marketing now help me both in tourism and in working with dogs. I combine all of it.”

Why Armenian journalists are leaving the profession

Why Armenian journalists are leaving the profession

Why Armenian journalists are leaving the profession

Why Armenian journalists are leaving the profession

today.az/news/politics/…

#Karabakh is internationally recognized as part of #Azerbaijan. Gratitude for 2016 events should acknowledge this reality, rather than framing occupation as heroism #InternationalLaw #SouthCaucasus #Peace #Diplomacy #Geopolitics #ConflictResolution— Today.Az (@TodayAz97) Apr 3, 2026

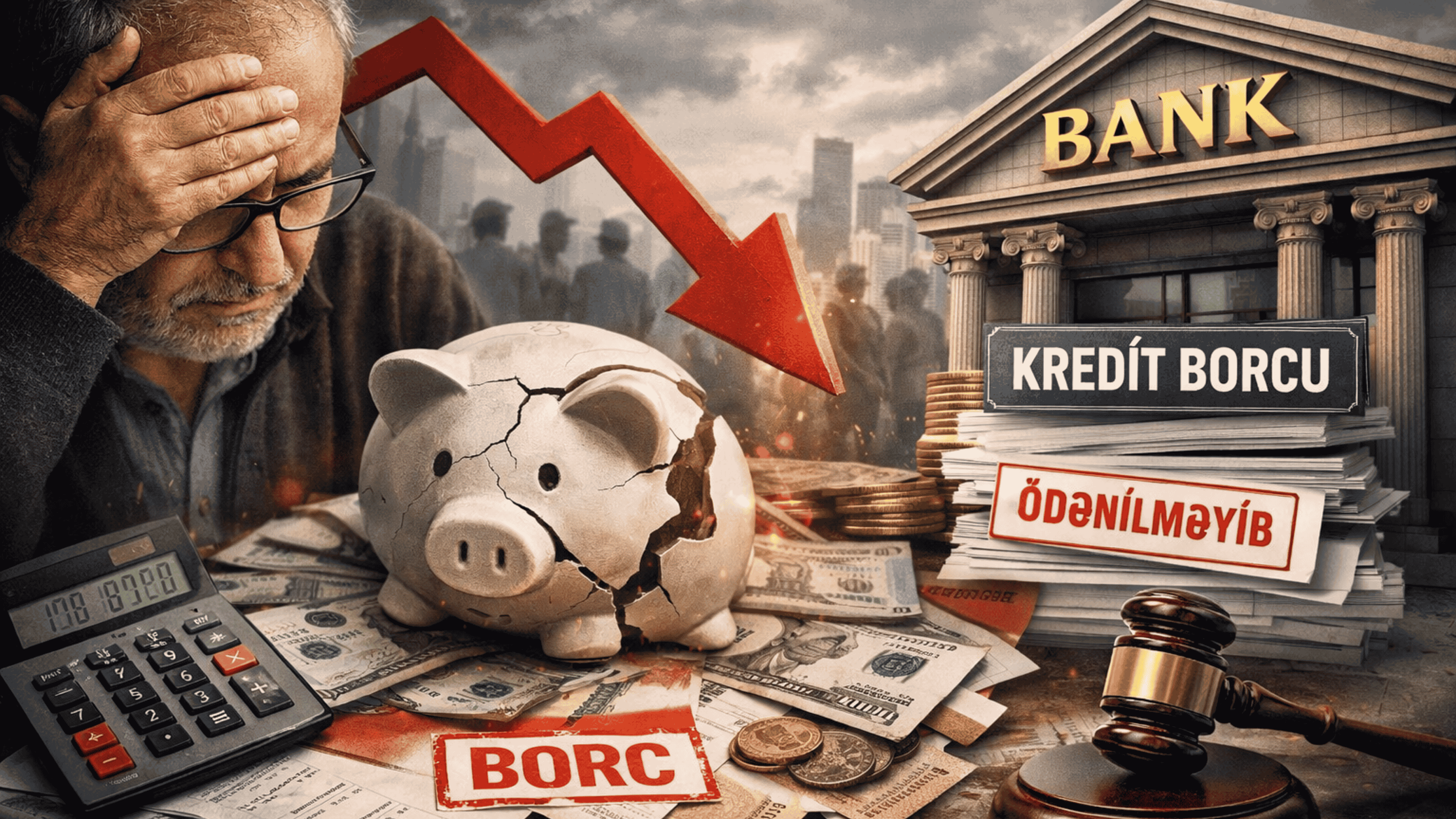

Non-performing loans in Azerbaijan

A non-performing loan is one where the payment deadline has passed but the borrower is unable to repay. For the borrower, it is a source of stress; for banks, a risk; and for the wider economy, a warning signal.

According to official statistics from the Central Bank of Azerbaijan under the indicator “loans of credit organisations”, the volume of overdue loans stood at 557.5 million manats (approximately $328 million) as of 1 February 2026.

By 1 March, this figure had risen to 562 million manats (around $330 million), marking an increase of about 0.8% compared with 1 February.

The annual trend also shows a notable rise. As of 1 March 2025, the volume of non-performing loans was 480.1 million manats (approximately $282.5 million). Compared with this, the March 2026 figure of 562 million manats represents an increase of around 17%.

What does past experience show?

The issue of non-performing loans in Azerbaijan did not emerge overnight. It is the result of several major waves over time.

One of the most significant occurred in the mid-2010s. In 2015, the manat sharply depreciated — a devaluation that made the national currency weaker while the US dollar strengthened.

How is devaluation linked to bad loans?

Imagine you took out a loan of $10,000. When the manat weakens, the equivalent value of that debt in the national currency increases. If your income is in manats but your debt is in dollars, repayment begins to feel as if the debt itself is growing.

This is why the volume of non-performing loans surged after 2015. A clear example is the figure recorded on 1 April 2017, when bad loans exceeded 1.59 billion manats (approximately $935.3 million).

The state later stepped in. In February 2019, a government mechanism was introduced to address part of the bad loan burden. It included compensating exchange rate differences on foreign currency loans held by individuals. The legal framework was based on presidential decrees aimed at resolving non-performing loans and setting out implementation mechanisms. Following this, the downward trend in bad loans became more pronounced.

This is reflected in the long-term data from the Central Bank of Azerbaijan. According to official statistics, overdue loans stood at 893.1 million manats in 2020 (approximately $525.4 million), 719.4 million in 2021 (around $423.2 million), 593.7 million in 2022 (about $349.3 million), and 437.8 million in 2023 (approximately $257.6 million). Over several years, this showed a steady decline.

However, the trend began to shift again in 2024. By the end of that year, the figures started rising once more, reaching 562 million manats as of 1 February 2026.

Why are non-performing loans rising?

There is rarely a single reason behind an increase in bad loans. More often, it is the result of several overlapping factors. At its simplest, the gap between people’s incomes and expenses is widening.

Inflation — the steady rise in prices — is felt in everyday life. The cost of bread, rent, transport, medicines and children’s needs is gradually increasing. At the same time, incomes — wages or daily earnings — are not growing at the same pace.

As a result, household budgets come under pressure. Experts frequently highlight this link, noting that weak growth in real incomes limits borrowers’ ability to repay and contributes to a rise in overdue loans.

A simple example illustrates the point. You take out a bank loan to buy a car, with a monthly payment of 450 manats (around $265). At the same time:

- fuel prices increase

- food costs rise

- school-related expenses appear

- spending on healthcare and medicines grows

Meanwhile, your salary remains unchanged or increases only slightly. In such a situation, the first missed payments often occur on the loan. Households prioritise essential needs — food, transport to work and utility bills — while loan repayments are delayed by a month or two. This is often where the problem begins.

A second important factor is the rapid expansion of consumer lending. Consumer loans are typically taken out for everyday needs or desires — buying furniture or a phone, financing home repairs, purchasing a car or covering wedding expenses. The higher the level of household indebtedness, the greater the risk that non-performing loans will increase.

A third factor is high interest rates. An interest rate is the price paid to a bank for using a loan. The higher the rate, the heavier the monthly repayment becomes.

Economist Natig Jafarli, explaining the situation, says that delays most often occur on consumer loans. According to him, interest rates are excessively high, and some borrowers try to cope by taking out loans from several banks at once. In other comments, he also notes that high rates on consumer lending create an additional financial burden for households.

A fourth factor is lenders’ approach to risk. In some cases, loans are issued too easily: fewer documents are required, checks are superficial, and a “take now, deal with it later” approach prevails.

The Central Bank of Azerbaijan requires banks to introduce early warning systems for non-performing loans and procedures to identify risks in a timely manner. The very existence of such requirements suggests that proactive risk management remains a key issue.

A fifth factor is business lending. When economic activity slows, sales decline and the cost of raw materials rises, making it harder for small businesses to service their debts on time. Official statistics also show that business loans account for a significant share of non-performing loans (NPLs).

What do economists and official data say?

Official statistics answer the question “how much?”, while experts are more focused on explaining “why?”.

First, it is important to clarify a key official term. Under the prudential framework of the Central Bank of Azerbaijan, a non-performing loan (NPL) is defined as a loan where payments on the principal or interest are overdue by more than 90 days. In other words, while “overdue loans” and NPLs may sound like synonyms, they are measured differently in statistics. Without understanding this distinction, the figures can be misleading.

For example, in the Central Bank’s statistical bulletin for January 2026, banks’ NPL portfolio is estimated at around 794 million manats (approximately $467 million), accounting for about 2.6% of the total loan portfolio. This suggests that while the problem exists, it is not at a level that would trigger systemic alarm.

This view aligns with that of MP Vugar Bayramov. He notes that if the share of problem loans were to reach a risky threshold — for example, exceeding 3% — it could be considered a serious issue. At present, he argues, the figure is not critical.

Economist Eldeniz Amirov takes a similarly cautious stance on the growth of consumer lending. In comments to Modern.az, he described the overall expansion of the loan portfolio as a positive development, while warning that a rising share of consumer loans could have negative consequences. In other words, lending itself is not the problem, but excessive debt accumulation increases risks.

Natig Jafarli, for his part, points to sharper concerns. He highlights high interest rates and the tendency of some borrowers to cover current expenses by taking out loans from multiple banks, both of which can increase arrears. At the same time, he argues that it is not entirely fair to place responsibility solely on borrowers: when incomes fall and expenses rise, people often resort to borrowing simply to cope.

The position of official institutions is more measured. The Central Bank of Azerbaijan has tightened requirements for banks’ risk management while also using tools such as capital buffers to support financial stability. In its 2024 report, the regulator noted that, amid rapid credit growth, it introduced a countercyclical capital buffer — a move that indirectly signals rising risks when the credit market begins to overheat.

What does this growth mean — and what can be done?

First, what does a rise in non-performing loans mean for ordinary people?

As noted earlier, it has several consequences:

- More pressure on household budgets. As arrears grow, penalties and additional interest accumulate.

- Debt spirals. People may take out new loans to repay old ones, creating a “snowball effect” where debt rises rapidly.

- Psychological strain. Collection calls, warnings and fears of legal action increase stress levels.

What does it mean for banks?

When issuing loans, banks already factor in the risk of non-repayment. But as bad loans increase, they are required to set aside provisions — essentially reserving part of their income. This reduces profitability and can limit their ability to issue new loans.

There are broader economic risks as well.

When banks become more cautious, lending conditions tighten and the overall volume of credit declines. This can slow business activity. Small businesses, in particular, may struggle to access financing, which in turn affects growth.

What can the state and regulators do?

There is no single solution, but several approaches stand out:

- Stronger risk assessment in banks. This includes more careful verification of borrowers’ income and better measurement of debt burdens, such as the ratio of monthly payments to income. The Central Bank’s requirement to introduce early warning systems is part of this effort.

- Improving market conditions. While interest rates are market-driven, greater transparency and competition in consumer lending could reduce the overall burden. Natig Jafarli has also argued that lowering interest costs could help stimulate economic activity.

- Financial literacy. Borrowers need to assess more carefully, before taking out a loan, whether they will realistically be able to repay it.

- Targeted support and restructuring. Assistance for vulnerable groups and mechanisms such as extending loan terms or revising repayment schedules can ease pressure. A previous example is the 2019 state programme compensating exchange rate differences on foreign currency loans.

Taken together, these measures do not eliminate the problem entirely, but they can reduce risks — both for individuals and for the financial system as a whole.

today.az/news/politics/…

#Russia–#Armenia tensions signal a geopolitical shift as Yerevan balances between Moscow and the West ahead of elections that could reshape its future. #SouthCaucasus #EU #EAEU #ForeignPolicy #Elections #PoliticalStrategy #GlobalPolitics #RegionalSecurity— Today.Az (@TodayAz97) Apr 3, 2026