Azerbaijani Foreign Minister Jeyhun Bayramov met with Simon Steele, Executive Secretary of the UN Framework Convention on Climate Change, Report informs citing MFA.

Day: February 1, 2024

There is no doubt that Iran’s regime is playing an important role in the ongoing crisis in the Middle East. But what many analysts and politicians are still puzzled about is the motivation behind the regime fanning the flames of war in the region.

The regime’s primary objective is “to divert attention from the precarious internal state of the regime and the volatile conditions within Iranian society,” writes the National Council of Resistance of Iran (NCRI) in its latest comprehensive analysis of the regime’s regional strategy. The regime is trying in vain to contain an explosive society and prevent the expansion of the network of the Iranian Resistance.

“In this challenging context, the regime’s recurring strategy is to export crises abroad—a tactic employed consistently over more than four decades,” the NCRI writes.

But while the regime is trying to project power abroad, its officials are admitting that the social and economic conditions in Iran are exposing the regime’s weakness. And no amount of repression will provide the regime with reprieve from the situation.

On January 13, the Secretary-General of the Islamic Iran Nation Party Azar Mansouri warned about the implications of skyrocketing inflation and wage decreases, which is affecting all strata of the society except for the ruling elite. “If we cannot describe this situation as insecurity, what term would be fitting for this trend of diminishing the resources available to people?” Mansouri said. “Recent multifaceted protests, spanning from December 2017 to November 2019 and September 2022, have demonstrated an underlying accumulation of dissatisfaction and anger beneath the surface of society, emerging during opportune moments.”

In January 2023, the Secretary-General of the Kargozaran Party, Hossein Marashi that “over 75% of the Iranian population expresses dissatisfaction” with the regime. “We have a significant dissatisfied population, a portion of whom actively protest in the streets, and a small fraction might resort to causing disturbances,” he said.

In July 2023, the Jomhouri Eslami newspaper warned regime officials “of the day when the army of the hungry rises against you.”

The regime has a history of resorting to foreign wars and fictitious enemies to avoid solving the country’s problems and to suppress any form of protest or dissent.

However, today, the regime has a bigger problem, which is the expansion of the organized resistance movement, notably the growth of the Resistance Units, the Iran-based network of the regime’s main nemesis, the People’s Mojahedin Organization of Iran (PMOI/MEK).

On a state-organized radio show in August 2023, Mehdi Rouhani Far, introduced as an expert in political affairs and terrorism, described the PMOI as “one of the most significant factors” in protests, which he called “tensions.”

“Anyone with government responsibilities, resources, and authority must pay extremely close attention, and is necessary to consider two key aspects: 1) The threat posed by the organization is much greater than before and 2) Developing an analysis of the reincarnation and transformation of this organization is of utmost importance,” he said.

Other officials have also admitted that the PMOI and its network have become an important source of concern for the regime. On June 24, 2022, the Director of Human Rights Matters of the regime’s Judiciary, Kazem Gharibabadi, said, “There is no meeting with ambassadors of European countries or delegations of European countries in which we do not bring up the issue of the Hypocrites.”

The NCRI report lays out the regime’s inability to handle Iran’s critical situation, which has resulted in the escalation of poverty, unemployment, and corruption. At the same time, the regime’s brutal methods, including an alarming uptick in executions, especially political executions, have not managed to reduce the critical conditions of the regime.

“Despite calls for a change of course from every faction, their collective tenure at the helm of the country’s political and socio-economic affairs has fallen short of meaningful action, leaving Iranians disillusioned,” the NCRI writes. “Therefore, Iranians have long passed beyond the regime’s internal factions. Public statements, even those blaming the regime’s leadership to display free speech, offer no solace and cannot save the regime from the imminent burst of outrage.”

Viewing the regime’s warmongering policies in this light proves that Tehran is not a power broker but a weak regime that is trying hard to hide its own weaknesses.

“Due to misunderstandings or the influence of the regime’s deceptive campaigns, the international community has failed to comprehend the true motives behind the regime’s illicit regional activities,” the NCRI writes. “For lasting peace in the Middle East, it is crucial to recognize that Tehran does not need a mere policy change but rather a complete regime change.”

By G. Patrick Lynch

Javier Milei arrived at the World Economic Forum last week and easily commanded the stage, rebuking Davos Man with wit and wisdom. While most of the attendees arrived in their private jets, Milei flew on a commercial flight sporting his signature sideburns and slightly mischievous smile. Along with his unique appearance another constant feature of Milei has been his dire warnings about the failures of collectivism. And frankly no other political leader at the event could say they know more about the dangers of collectivist political economies than the new Argentine leader.

If you’ve never watched one of Milei’s speeches or television appearances, I strongly urge you to do so. The breadth of his knowledge about economic history and theory is remarkable and on evident display. You will be moved by the passion he brings to his discussions and presentations, and left wondering why other political leaders can’t match his abilities and energy. Politicians aren’t dumb, far from it, but their idealism tends to erode as they chase votes leaving their principles behind. Not Milei. He may not succeed in his mission to dismantle the sclerotic bureaucracy and dysfunctional central bank of Argentina, but he’s been unwaveringly clear about what he believes and what he’s trying to do. He’s trying to save Argentina from almost a century of exploitative and destructive fiscal and monetary governance.

At Davos he began by presenting the case that Angus Deaton has made about the importance of market systems in promoting economic development since 1800. He also cited, by name, Israel Kirzner, and sounded almost like Ayn Rand when describing heroic entrepreneurs and parasitic state actors and bureaucrats. Milei rightly defended the importance of considering government failure and rejected neoclassical claims of pervasive market failures. It’s almost as if the Mont Pelerin Society were his audience, not Davos. (Click here for a transcript of Javier Milei’s speech at Davos)

The international media have tried to link Milei to Former President Donald Trump, right wing populism, and other anti-establishment politicians. There’s little doubt Milei is taking on Argentina’s elites, and Mr. Trump and his supporters are broadcasting a similar anti-elite message to anyone who will listen. It’s also true that Trump and so many of his supporters (such as Heritage Foundation president Kevin Roberts, who also spoke at the World Economic Forum) have tried to embrace Milei with complimentary comments at Davos and on social media. Though the Trump camp might align themselves with Milei, the policy offerings from the economic nationalists bear little, if any, resemblance to the economic courage of the Argentine upstart. Rather than the thin gruel of economic grievance offered by American right-wing populists, Milei’s policies are built on his vast knowledge of sound and successful, albeit politically unpopular, economic thinking.

Milei’s ideas are a consistent set of interlocking principles based on an unqualified commitment to free markets in a classical liberal political economy. He, along with millions of Argentines, have experienced for years how significant government intervention severely damages an economy. After his victory on a platform of reversing that thievery and mismanagement, Milei must now confront the entrenched interests that have benefited from this vast web of crony capitalism. Milei will be lucky if he can simply stop the bleeding and redirect Argentina in a different direction.

Our GOP mouthpieces want to tell you that they are doing the same thing against the “deep state” who purportedly stole an election from President Trump in 2020 and are hurting Americans with elitist economic ideas about free trade and immigration. And America does face significant challenges, but the issues they cite are not the cause of our problems. The ideas of the economic nationalists in the US and elsewhere are hopelessly contradictory, politically expedient, short-term slogans to win an election and inflame passions. There is no underlying theory or consistent foundation to their hodgepodge of policies selected exclusively to please blue-collar voters in key electoral college states in 2024. If there is any underlying theory to these economic nationalist ideas it is collectivism, the exact danger that Milei himself identified in his speech.

Contrast Milei’s intervention at Davos with Kevin Roberts, whose comments at the Davos summit constitute little more than a laundry list of issues that appear to have been bounced off of focus groups for key voters in swing states. At the top is immigration. Roberts said the next conservative president will “take on” elites on behalf of “the average American.” He promises a Republican president would stand up to China, which he described as the “number one adversary to free people on planet Earth.” Presumably more tariffs will dispatch the Chinese, similar to Trump’s first term. It’s interesting that while conservatives are no longer globalists on topics like Ukraine, they apparently are “planetary” in their concerns.

None of these issues are consistent with free markets and liberty oriented economic policies. Argentina has long had one of the most open immigration policies on the planet; it has struggled with free trade, which remains a key factor in producing growth, as much as some people wish to distort the facts about that.

Milei’s popularity among young people throughout Latin America owes to the spark of hope he’s provided to them in countries mired for years in the exact political interference that the economic nationalists wish to expand. Just because something polls well in Michigan and Ohio doesn’t mean it’s right, moral, or consistent with growth, freedom, and prosperity. Perhaps Milei’s style and substance could rub off on Trump and the conservative populists. Instead of trying to claim him, they might endeavor to learn from him.

- About the author: G. Patrick Lynch is a Senior Fellow at Liberty Fund.

- Source: This article was published by AIER

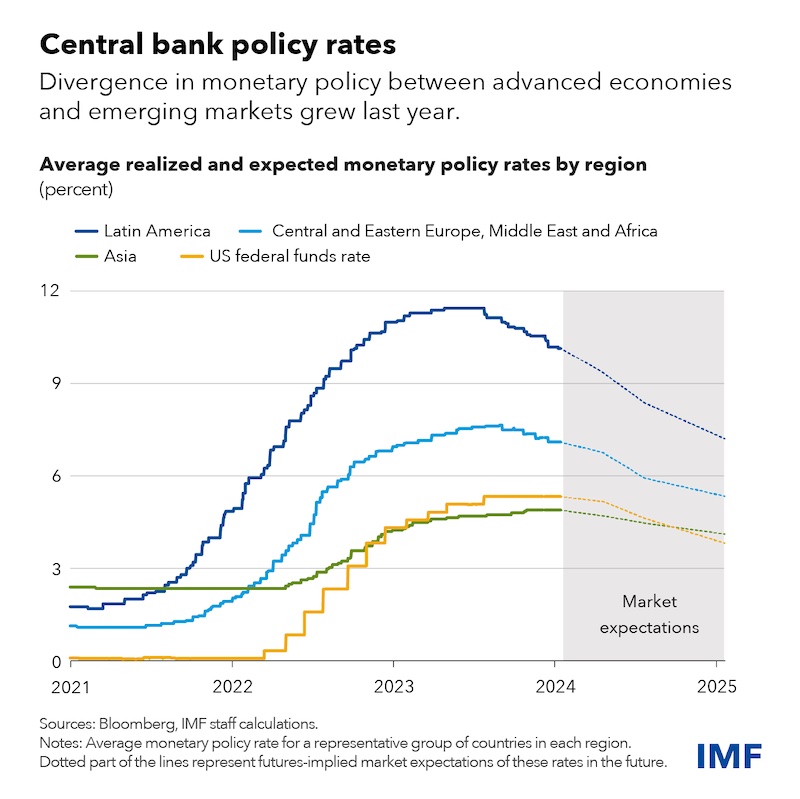

Global interest rates in recent months have gone on a rollercoaster, especially those on longer-term government bonds. Yields on 10-year US Treasuries are climbing again after pulling back from a 16-year high of 5 percent in October. Interest rate moves in other advanced economies had been equally prodigious.

Emerging market economies, however, saw much milder rate moves. We take a longer-term perspective on this in our latest Global Financial Stability Report, demonstrating that the average sensitivity to US interest rates of 10-year sovereign yield of Latin American and Asian emerging markets declined by two-thirds and two-fifths, respectively, during the current monetary policy tightening cycle compared with the taper tantrum in 2013.

While the lower sensitivity is in part due to the divergence in monetary policy between advanced economies’ and emerging markets’ central banks over the past two years, it nonetheless challenges findings in the economic literature that show large spillovers from advanced economies’ interest rates to emerging markets. In particular, major emerging markets have been more insulated from global interest rate volatility than would be expected based on historical experience, especially in Asia.

There are other signs of resilience in major emerging markets during this period of volatility. Exchange rates, stock prices, and sovereign spreads fluctuated in a modest range. More remarkably, foreign investors did not leave their bond markets, in contrast to past episodes when large outflows ensued after surges in global interest rate volatility, including as recently as 2022.

This resilience was not just good luck. Many emerging markets have spent years improving policy frameworks to mitigate external pressures. They have built additional currency reserves over the last two decades. Many countries have refined exchange-rate arrangements and moved towards exchange-rate flexibility. Significant foreign exchange swings have contributed to macroeconomic stability in many cases. The structure of public debt has also become more resilient, and both domestic savers and domestic investors have become more confident investing in local-currency assets, reducing reliance on foreign capital.

Perhaps most importantly, and closely aligned with IMF advice, major emerging markets have enhanced central bank independence, improved policy frameworks, and gained progressively more credibility. We would also argue that central banks in these countries have gained additional credibility since the onset of the pandemic by tightening monetary policy in a timely manner and bringing inflation toward target as a result.

During the post-pandemic era, many central banks hiked interest rates earlier than counterparts in advanced economies—on average, emerging markets added 780 basis points to monetary policy rates compared to an increase of 400 basis points for advanced economies. The wider interest differentials for those emerging markets that hiked rates created buffers for emerging markets that kept external pressures at bay. In addition, the rise in prices of commodities during the pandemic also helped the external positions of commodity-producing emerging markets.

Global financial conditions too have remained quite benign during the current global monetary policy tightening cycle, especially last year. This contrasts with previous hiking episodes in advanced economies, which were accompanied by a much more pronounced tightening of global financial conditions.

Looking ahead

Despite reaping rewards from years of building buffers and pursuing proactive policies, policymakers in major emerging markets need to stay vigilant with an eye on the challenges inherent in the “last mile” of disinflation and rising economic and financial fragmentation. Three challenges stand out:

- Interest rate differentials are narrowing as some emerging markets are anticipated by investors to cut rates faster than advanced economies, which could entice capital to leave emerging market assets in favor of assets in advanced economies;

- Quantitative tightening by major advanced economies continues to withdraw liquidity from financial markets, which could additionally weigh on emerging market capital flows;

- Global interest rates remain volatile, as investors—reacting to central banks emphasizing data-dependency—have grown more attentive to surprises in economic data. Perilous for emerging markets are market projections that central banks in advanced economies will materially cut rates this year. Should this prove wrong, investors may once again reprice in higher-for-longer rates, weighing on risky asset prices, including emerging market stocks and bonds.

A slowdown in emerging markets, as projected by the latest World Economic Outlook update, operates not only through traditional trade channels, but also through financial channels. This is particularly relevant now, as more borrowers globally are defaulting on loans, in turn weakening banks’ balance sheets. Emerging market bank loan losses are sensitive to weak economic growth, as we showed in a chapter of the October Global Financial Stability Report.

Frontier emerging markets—developing economies with small-but-investable financial markets—and lower-income countries face greater challenges, the primary one being the lack of external financing. Borrowing costs are still high enough to effectively prohibit these economies from obtaining new financing or rolling over existing debt with foreign investors.

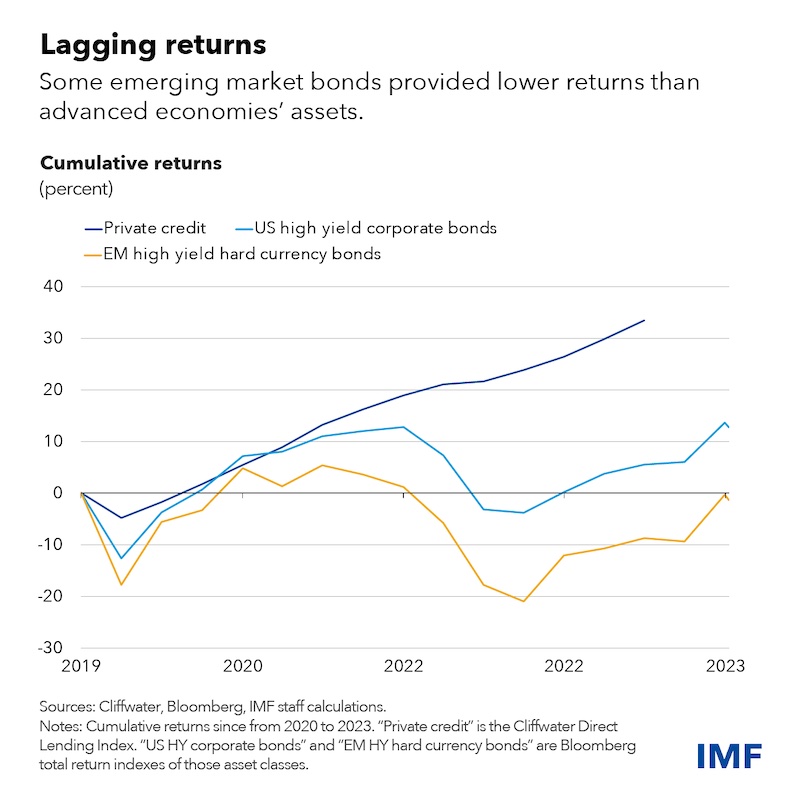

High financing costs reflect the risks associated with emerging market assets. Indeed, the dollar returns on these assets have lagged similar advanced economies’ assets during this high-rate environment. For instance, emerging market bonds for high-yield, or lower-rated, issuers have returned about zero percent on net over the past four years, while US high-yield bonds have provided 10 percent. So-called private credit loans provided by nonbanks to lower-rated US companies have returned even more. The sizable differences in returns may not bode well for emerging markets’ external financing prospects as foreign investors with mandates that allow for investments across asset classes can find more-profitable alternative assets in advanced economies.

While these challenges for emerging market and frontier economies require close attention by policymakers, there are also many opportunities. Emerging markets continue to see significantly higher expected growth rates than advanced economies; capital flows to stock and bond markets remain strong; and policy frameworks are improving in many countries. Hence the resilience of major emerging markets that has been important for global investors since the pandemic may continue.

Vigilant policies

Emerging markets should continue to build on the policy credibility they have gained and be vigilant. Facing elevated global interest rate volatility, their central banks should continue to commit to inflation targeting, while remaining data dependent in their inflation objectives.

Keeping monetary policy focused on price stability also means using the full spate of macroeconomic tools to fend off external pressures, with the IMF’s Integrated Policy Framework providing guidance on the use of currency intervention and macroprudential measures.

Frontier economies and low-income countries could strengthen engagement with creditors—including through multilateral cooperation—and rebuild financial buffers to regain access to global capital. In the bigger picture, countries with credible medium-term fiscal plans and monetary policy frameworks will be better positioned to navigate periods of global interest rate volatility.

About the authors:

- Tobias Adrian is the Financial Counsellor and Director of the IMF’s Monetary and Capital Markets Department. He leads the IMF’s work on financial sector surveillance and capacity building, monetary and macroprudential policies, financial regulation, debt management, and capital markets.

- Fabio M. Natalucci is a Deputy Director of the Monetary and Capital Markets Department with responsibility for the IMF’s global financial markets monitoring and systemic risk assessment functions. He oversees the Global Financial Stability Report that gives the IMF’s assessment of global financial stability risks. He is also responsible for monitoring and evaluating risks and opportunities in sustainable finance markets.

- Jason Wu is the assistant director overseeing the Global Markets and Analysis division at the IMF. Prior to joining the IMF, he held senior positions in the Federal Reserve Board’s Monetary Affairs and International Finance divisions.

Source: This article was published by IMF Blog

By Kung Chan and Xia Ri

Since the outbreak of the COVID-19 pandemic in 2020, the United States has implemented large-scale cash subsidies, various tax reductions, and wage protection plans. Notably, the Coronavirus Aid, Relief, and Economic Security (CARES) Act in March 2020 provided USD 1200 per person, the COVID-Related Tax Relief (CRTR) Act in December 2020 allocated USD 600 per person, and the ARP (American Rescue Plan) Act in March 2021 distributed USD 1400 per person. Simultaneously, the Federal Reserve initiated quantitative easing, swiftly lowering interest rates to zero through two emergency operations, maintaining this stance until March 2022.

According to the basic principles of economics, the U.S. should experience significant inflation in the later stages. However, to the perplexity of economists globally, the country is undergoing high growth with low inflation. Recent initial estimates from the U.S. Department of Commerce indicate a 2.5% economic growth for the whole year of 2023, surpassing the 1.9% growth in 2022. Based on FactSet’s consensus estimate, economists predict a slight increase in the overall annual inflation rate for 2023, rising from the previous month’s 3.1% to 3.2%. Notably, the consumer-level annual inflation has significantly decreased from December 2022’s 6.5%.

Meanwhile, the Fed continues to raise interest rates. In 2023, the Fed held its customary eight regular interest rate meetings. Among them, four meetings opted for rate hikes, and four meetings maintained the rates unchanged. According to statistics, starting from March 2022, when this round of interest rate hikes began, by July 2023, it had raised rates 11 times, accumulating an increase of 525 basis points. Although multiple rate hikes have caused the pain of declining economic growth, the Fed deems it necessary and worthwhile, believing it significantly aids in keeping inflation below 2%. How to explain this phenomenon of “high growth, low inflation”?

ANBOUND’s founder Kung Chan believes that the key factor is the robustness of the U.S. labor market. It has increased residents’ income and consumption, elevated economic growth rates, supported the U.S. dollar exchange rate, made imported goods cheaper, and restrained inflation.

In the context of deglobalization, the U.S. has implemented numerous industrial and technology policies, with many industries and sectors returning to the country, aligning with the “Make America Great Again” (MAGA) trend. Notably, the U.S. government has issued four major acts, including the ARP Act, Infrastructure Investment and Jobs Act (IIJA), CHIPS and Science Act, and Inflation Reduction Act (IRA), providing approximately USD 550 billion in support for industries like chips and new energy vehicles. The total expenditure could reach USD 1.3 trillion in the future.

These technology industry policies have resulted in significant growth in U.S. manufacturing construction spending and real investment. As of September 2023, seasonally adjusted annualized construction spending reached USD 19.965 trillion, a YoY increase of 8.7%, primarily driven by substantial growth in manufacturing spending, contributing 48% to the overall growth. Monthly YoY growth rates have consistently exceeded 60% since the beginning of 2023.

In this situation, while the U.S. labor market is very robust, it still witnesses a decrease due to multiple interest rate hikes, maintaining an overall high level throughout the year. According to data from the U.S. Department of Labor, the total number of new jobs in 2023 was 2.7 million, with an average monthly increase of 225,000, a growth rate higher than before the COVID-19 pandemic. The government, healthcare, leisure, and hospitality industries are the main sectors driving employment growth. In 2023, the government added an average of 56,000 jobs per month, more than twice the average of 23,000 jobs per month in 2022. However, looking at the number of new jobs added for three consecutive months, it had dropped to 165,000 by the end of 2023, reaching a new low since January 2021 and far below the 334,000 at the beginning of 2023.

Additionally, in December 2023, the U.S. labor force participation rate was 62.5%, nearly unchanged from the beginning of the year at 62.4%, maintaining a high level throughout the year, with a 0.8 percentage point gap compared to February 2020. The U.S. unemployment rate increased from 3.4% at the beginning of 2023 to 3.7%, a rise of 0.3 percentage points. However, in a historical context, the unemployment rate still remains within historically low levels. Monthly wages for December also saw a slight increase: the average hourly earnings for non-farm employees in the U.S. rose by 0.4%, reaching USD 34.27. Over the past 12 months, average hourly earnings have grown by 4.1%.

Due to the increase in employment rates and wage growth, American residents’ income has significantly risen, supporting the rapid growth of annual consumption, albeit with some fluctuations. According to relevant data, the U.S. consumer spending indicators for the fourth quarter of 2023 mostly declined compared to the previous quarter, with a seasonally adjusted annual rate of 2.8%, showing a decrease from the previous quarter but still surpassing market expectations. Against the backdrop of a lower base in the same period last year, the year-on-year growth rate of consumption reached 2.6%, up by 0.4 percentage points from the previous quarter. In particular, the month-on-month adjusted annual rate for goods fell to 3.8%, benefiting from increased consumer demand during the year-end holiday season, including Black Friday and Christmas, and still maintained positive growth. Meanwhile, the month-on-month adjusted annual rate for services rose to 2.4%, up by 0.2% from the previous quarter, becoming a major driving force for consumption.

The growth in consumer spending has supported a high economic growth rate, subsequently bolstering the U.S. dollar exchange rate, making goods cheaper and suppressing inflation. With expectations of interest rate cuts, American residents’ consumption may further increase, continuing to support the economic growth of the country. According to data from the University of Michigan, the U.S. consumer confidence index soared to 78.8 in January 2024, reaching the highest level since July 2021 and experiencing a 29% surge since November 2023, marking the largest two-month increase since 1991, indicating an improvement in consumer sentiment.

Final analysis conclusion:

Currently, the U.S. is experiencing high growth coupled with low inflation, a phenomenon that has left economists worldwide incredulous and perplexed. Despite causing the pain of declining economic growth, the Fed’s multiple interest rate hikes have been highly effective in suppressing inflation. More importantly, leveraging geopolitical dynamics and formulating policies in the technology sector, the U.S. has attracted a significant influx of industries and production, leading to a booming labor market. This, in turn, has increased American residents’ income and consumption, boosted economic growth rates, supported the U.S. dollar exchange rate, made imported goods cheaper, and further restrained inflation.

Kung Chan and Xia Ri are researchers at ANBOUND