India-Armenia hold bilateral talks during 10th Foreign Office … Business Standard

Day: November 18, 2023

By He Jun

On November 15, China’s National Bureau of Statistics released the latest economic data for October. From the data, the economic performance in the first month of the fourth quarter can essentially reflect the overall economic situation for the entire quarter, indicating that the general framework of the country’s economy in 2023 has been largely determined.

In terms of industry, the value-added of industries above the designated size increased by 4.6% year-on-year (y-o-y) in October, accelerating by 0.1 percentage points compared to the previous month. Looking at three major categories, the value-added of the mining industry increased by 2.9% y-o-y, manufacturing grew by 5.1%, and the production and supply of electricity, heat, gas, and water increased by 1.5%. By economic type, the value-added of state-owned holding enterprises increased by 4.9% y-o-y; shareholding enterprises grew by 5.6%, foreign and Hong Kong, Macao, and Taiwan-invested enterprises grew by 0.9%, and private enterprises increased by 3.9%. In terms of products, the output of solar cells, service robots, and integrated circuit products increased by 62.8%, 59.1%, and 34.5% y-o-y, respectively. From January to October, the value-added of industries above a designated size increased by 4.1% y-o-y. From January to September, the total profit of industrial enterprises above the designated size nationwide decreased by 9.0% y-o-y. In October, the Purchasing Managers’ Index (PMI) for the manufacturing industry was 49.5%, while the business activity expectation index was 55.6%.

It should be pointed out that the industrial sector is experiencing a slower recovery this year. The overall Chinese economic situation is not exactly favorable, coupled with the global restructuring of the supply chain and the relocation of industrial chains, resulting in mediocre performance in the country’s domestic industry. The growth rate of industrial value-added stabilized in October; at the same time, given the industrial downturn in the last two months of the previous year, there is a possibility of a slight increase in industrial value-added data in the last two months of this year. The annual growth rate of value-added in large-scale industries may exceed 4.1%. Yet, noteworthily the profits of industrial enterprises are in negative growth, and they may not necessarily turn positive for the whole year. This year, the challenges faced by enterprises are evident, particularly in the industrial sector.

Figure 1: Year-on-year Growth Rate of Value-Added in Industries above Designated Size

Source: National Bureau of Statistics

Source: National Bureau of Statistics

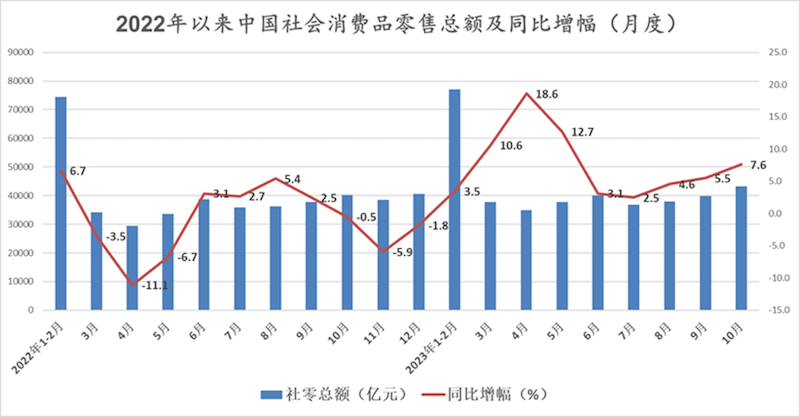

In terms of consumption, in October, the total retail sales of social consumer goods reached RMB 43,333 billion, a y-o-y increase of 7.6%, accelerating by 2.1 percentage points compared to the previous month. By consumption type, retail sales of goods amounted to RMB 38,533 billion, with a y-o-y growth of 6.5%, while F&B revenue reached RMB 480 billion, marking a y-o-y growth of 17.1%. Among the retail sales of goods in enterprises above the designated size, sports and entertainment goods, communication equipment, automobiles, and precious metals and jewelry saw increases of 25.7%, 14.6%, 11.4%, and 10.4%, respectively. From January to October, the total retail sales of social consumer goods amounted to RMB 385,440 billion, with a y-o-y increase of 6.9%. The national online retail sales reached RMB 122,915 billion, reflecting an 11.2% y-o-y increase. In the first ten months, the y-o-y growth of service retail sales was 19.0%, accelerating by 0.1 percentage points compared to the period from January to September.

From the data, it can be observed that consumer spending in October has started to recover significantly from the lows in August and September. However, the rebound in October is influenced by seasonal factors, with the so-called Golden Week long holidays playing a crucial role in supporting consumption growth during this month. Last year, the performance of consumer spending in the last two months was mediocre, and under the base effect, the y-o-y growth of consumption in the last two months of this year may continue to rise. If there are no unexpected factors, the y-o-y growth of consumption for the whole year may exceed 7%. Overall, the actual recovery of consumption this year is not as expected. Still, due to lackluster export performance and a trend of slowing investment growth, the contribution of consumption to this year’s economic growth may reach a high level.

Figure 2: Total Retail Sales of Consumer Goods in China and Year-on-Year Growth Rate (Monthly) since 2022.

Source: National Bureau of Statistics. Chart plotted by ANBOUND.

Source: National Bureau of Statistics. Chart plotted by ANBOUND.

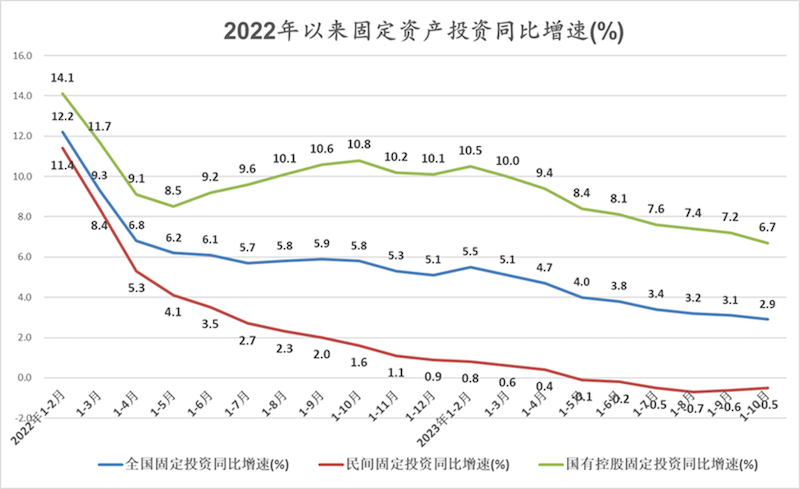

When it comes to investment, from January to October, the total fixed asset investment nationwide (excluding rural households) was RMB 41,940.9 billion, a y-o-y increase of 2.9%, down 0.2 percentage points from January to September. Breaking it down by sector, infrastructure investment increased by 5.9% y-o-y, manufacturing investment rose by 6.2%, and real estate development investment decreased by 9.3%. The national sales area of commercial buildings was 925.79 million square meters, a y-o-y decrease of 7.8%. The sales value of commercial buildings was RMB 97,161 billion, a drop of 4.9%. By industry, investment in the primary industry decreased by 1.3% y-o-y, investment in the secondary industry increased by 9.0%, and investment in the tertiary industry grew by 0.4%. Private investment decreased by 0.5%, narrowing down by 0.1 percentage points compared to January-September; state-controlled investment increased by 6.7%, with the growth rate continuing to slow down. Excluding real estate development investment, private investment increased by 9.1% y-o-y. Investment in high-tech industries grew by 11.1% y-o-y in October, and month-on-month (m-o-m) fixed asset investment (excluding rural households) increased by 0.10%.

Investment has been a relatively underperforming sector in the economy this year. Despite the country introducing numerous policies and initiating several major projects to stabilize the economy, the investment growth rate continues to decline persistently, with private investment experiencing six consecutive months of negative growth. The subdued investment reflects a significant lack of domestic demand this year, especially with severe deficiencies in business confidence. It is worth noting that China’s domestic investment downturn is significantly influenced by the decline in real estate investment, with a substantial portion of private investment concentrated in the real estate sector. The structural changes observed in fixed asset investment imply that the future recovery of investment growth will depend on whether real estate investment can stabilize. Some argue that market confidence primarily relies on consumption, but according to researchers at ANBOUND, whether the Chinese market has confidence in 2023 primarily depends on investment and enterprises. After October, most of the projects that needed investment have been completed. Even with additional investment, it is difficult to contribute significantly to this year’s GDP. In the last two months, the national investment growth rate may slow down slightly, and the annual investment growth rate may be between 2-3%. We also believe that the sluggish trend in fixed asset investment this year may continue into early next year. It is crucial to emphasize that the significant deviation between the investment cycle and the policy cycle this year demonstrates the powerful inertia of market adjustments which are not easily swayed by policy intentions.

Figure 3: Year-on-Year Growth Rate of Fixed Asset Investment since 2022 (%)

Source: National Bureau of Statistics. Chart plotted by ANBOUND.

Source: National Bureau of Statistics. Chart plotted by ANBOUND.

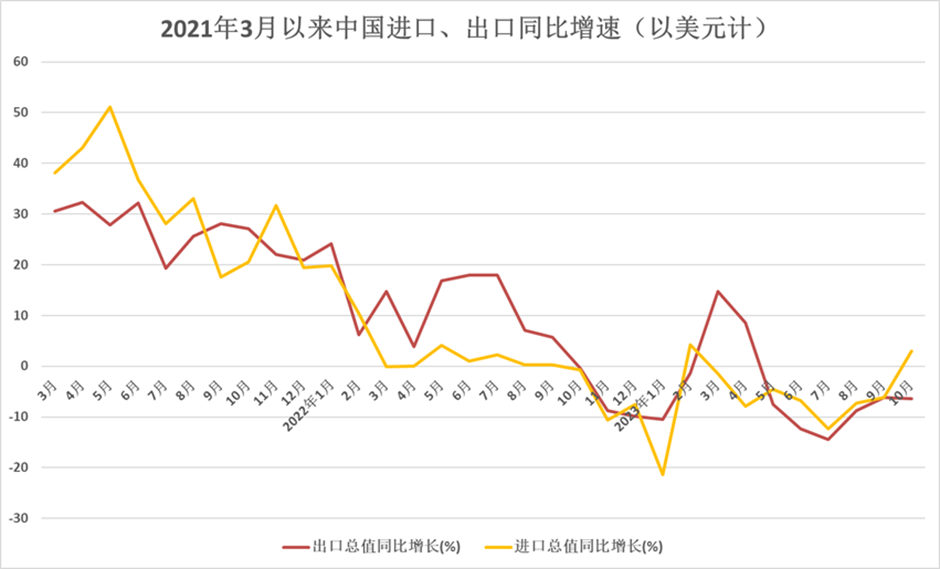

As for foreign trade, in October, the total value of goods imported and exported was RMB 35,417 billion, a y-o-y increase of 0.9%. Among them, exports were RMB 19,736 billion, a decrease of 3.1%, and imports were RMB 15,681 billion, an increase of 6.4%. After offsetting imports and exports, the trade surplus was RMB 405.5 billion. In terms of USD, in October of this year, China’s total imports and exports were USD 493.13 billion, a decrease of 2.5%. Among them, exports were USD 274.83 billion, a decrease of 6.4%, and imports were USD 218.3 billion, an increase of 3%. The trade surplus was USD 56.53 billion, narrowing by 30.8%. From January to October, the total value of goods imported and exported was RMB 34.32 trillion, a y-o-y increase of 0.03%. Among them, exports were RMB 19.55 trillion, an increase of 0.4%, and imports were RMB 14.77 trillion, a decrease of 0.5%. The trade surplus was RMB 4.78 trillion, expanding by 3.2%. However, in terms of USD too, in the first 10 months of this year, the country’s total imports and exports were USD 4.9 trillion, a decrease of 6%. Among them, exports were USD 2.79 trillion, a decrease of 5.6%, and imports were USD 2.11 trillion, a decrease of 6.5%. The trade surplus was USD 684.04 billion, narrowing by 2.7%.

From a macro perspective, China’s imports and exports are in a downward trend, which, although related to the overall environment of global economic slowdown and weak demand, also indicates a worrisome trend—the contraction of the country’s relationship with the world economy and the ongoing “progressive decoupling” in the trade sector. Researchers at ANBOUND have been concerned that a new process of globalization is underway, and China may lack a position in it. The latest changes in China’s foreign trade can provide a glimpse of this evolving trend.

Figure 4: China’s Import and Export Year-on-Year Growth Rates (In USD) Since March 2021

Source: National Bureau of Statistics. Chart plotted by ANBOUND.

Source: National Bureau of Statistics. Chart plotted by ANBOUND.

In terms of prices, in October, the national consumer price index (CPI) decreased by 0.2% y-o-y and 0.1% m-o-m. From January to October, the national consumer price index rose by 0.4% y-o-y. In October, the national producer price index (PPI) decreased by 2.6% y-o-y, remaining unchanged m-o-m The national industrial producer purchase prices decreased by 3.7% y-o-y and increased by 0.2% m-o-m. From January to October, the national industrial producer ex-factory prices and purchase prices decreased by 3.1% and 3.6% y-o-y, respectively. Looking at the overall trend presented by CPI and PPI data, the activity levels in both consumption and production remain relatively low this year.

Final analysis conclusion:

From the economic data of the first 10 months, the Chinese economic cycle appears to be inconsistent with the policy cycle, indicating a strong inertia in economic operation that does not shift with policy changes. With less than two months left until the end of 2023, the overall economic situation is largely determined. In terms of policies, the focus should be on maintaining stability, without the need to aggressively expand investment or initiate new projects. It is essential to reserve resources for the economic challenges of the coming year. Furthermore, the future economic policy of the country should continue to concentrate on people’s livelihoods and the consumer sector, supporting the development of private enterprises.

He Jun is a researcher at ANBOUND

Vietnam has actively pursued its major expansion plan in the disputed South China Sea, nearly doubling newly-reclaimed areas in one year, a new report said.

Since December 2022, “Vietnam has created another 330 acres [133.5 hectares] of land” on rocks and reefs within the Spratly archipelago, according to the report by the Asia Maritime Transparency Initiative, or AMTI, at the U.S. Center for Strategic and International Studies, or CSIS, think tank.

That was in addition to the 420 acres (170 hectares) reclaimed in 2022.

“By contrast, Vietnam had created just 120 acres [48 hectares] of land in the Spratlys between 2012 and 2022,” the report said.

“This all adds up to about a quarter of the more than 3,200 acres [1,295 hectares] of land created by China from 2013 to 2016, but it is far more island expansion than any other claimant besides China has undertaken.”

The report looked into five Vietnamese outposts in the sea, including Barque Canada Reef which “has undergone the largest transformation by far.”

Last week Radio Free Asia reported on the remarkable pace of reclamation on the reef.

“Formerly one of Vietnam’s smallest outposts, over 210 acres [85 hectares] of new land have been created at Barque Canada in the last year, making it now the largest Vietnamese-occupied feature in the South China Sea,” AMTI’s report said.

Other features that have been built up rapidly are Pearson Reef, Namyit Island, Sand Cay and Tennent Reef.

AMTI said dredging and landfill have also continued, though at a smaller scale, at Alison Reef, Cornwallis South Reef, Ladd Reef, and Discovery Great Reef, indicating that “a major expansion of any of these reefs in the future cannot be ruled out.”

The report noted that the focus of Vietnam’s efforts remains “primarily on dredging and landfill, with construction of infrastructure yet to begin in earnest at most features.”

Cutter suction dredgers

While examining satellite imagery, AMTI researchers discovered that in order to accelerate its dredging efforts, “Vietnam has turned to a tool that it had previously shied away from: cutter suction dredgers.”

A cutter suction dredger cuts hard soil or rock on the seabed into fragments with a rotating head. The material is then sucked up by dredge pumps and discharged to a deposit area through pipelines across sea and land.

At Barque Canada Reef on Nov. 2, 2023, at least two such dredgers could be seen clearly on the image provided by the U.S. satellite imaging company Planet Labs. Another two were present at Pearson Reef on Oct. 27, 2023.

They “are of the same type that China was criticized for using during its island-building campaign in 2014-2017 due to their outsize ecological impact,” the report said.

Dredging can be harmful to the marine environment due to physical effects on coral and seagrass, said Victoria Todd, Managing Director & Chief Scientist at Ocean Science Consulting Ltd.

“Collisions, noise production, and increased seabed disturbance can affect marine life directly,” she told RFA.

“Indirectly, changes in environment characteristics, such as topography, depth, sediment particle size … can also affect them,” Todd said, adding that the issue is “highly complex and should be studied carefully.”

“How much and how long-term the impacts are very much depends on where and how dredging is being carried out.”

Previously, Vietnam used clamshell dredgers and construction equipment to scoop up sections of shallow reef and deposit the sediment on the landfill areas. This method is considered more time-consuming but less destructive than cutter suction dredging.

“The use of cutter suction dredgers is worrying because they are more environmentally destructive than traditional methods, but even more so because they risk playing into China’s information operations,” said Greg Poling, AMTI’s director.

Information battle

“This round of land reclamation is just at the beginning,” said the Chinese think tank South China Sea Probing Initiative (SCSPI) on the social media platform X previously known as Twitter.

“Ever since 1970s, Vietnam has never stopped expanding its outposts in Spratly Islands,” SCSPI added.

China has developed and fully militarized three artificial islands in the South China Sea, including Mischief Reef, Subi Reef and Fiery Cross, with missile arsenals, airfields and aircraft hangars, radar systems and other military facilities.

Yet “Chinese actors are trying to paint Vietnam as the one really militarizing and destabilizing the South China Sea,” said AMTI’s Poling.

“Vietnam appears to only be using these kinds of dredgers to create new harbors and for the major expansion of Barque Canada, so it’s still a much smaller environmental impact than China’s dredging had.”

“But that nuance could be lost in the narrative battle between Beijing and Hanoi,” warned the maritime analyst.

The Vietnamese government has yet to say anything about the AMTI report but Hanoi’s official stance has been that it only carries out works to protect the features but not to expand or change the structures of islands under its control.

“There is a saying in Vietnamese: ‘When you meet with Buddha, wear a monk’s robe but when you see a ghost, put on a paper dress’, which means: When in Rome do what the Romans do,” said Song Phan, a Sydney-based South China Sea researcher.

“Many of my colleagues think it is not advisable for Vietnam to sit idle when its big neighbor is behaving so assertively,” Song added.. “I don’t necessarily agree with them though. In my opinion, all sides need to strive to preserve the status quo in the sea.”

The apparent island-building campaign, however, has become a hot topic on internet forums in Vietnam, with netizens praising the government’s efforts.

“Worth every penny,” reads a comment by Dung Nguyen on a defense forum called Truong Sa Ngay Moi.

“Hope we can accelerate the island expansion even faster before our “friend” decides to disrupt it,” said another blogger, Hieu Do Van.

The 2023 Nobel Prize in Economics was awarded to the famous American economist, Harvard University Professor Claudia Goldin. Her subject of study is women and the gender gap in labour markets. Since the Nobel Prize in Economics began in 1969, only two women, Elinor Ostrom in 2009 and Esther Duflo in 2019, have received the honour.

And now, in 2023, Professor Goldin has been honored again for her work on challenges and success in women’s labour markets. She has done an in-depth analysis of the trends and nature of women in the labour market. Goldin’s research does not offer solutions alone; it also allows policymakers to tackle the entrenched problem.

Goldin’s study explains that a woman’s position in the labour market and her corresponding income are not solely shaped by overarching societal and economic changes. They are also influenced, in part, by her personal choices, such as the level of education she pursues. The work of Professor Goldin seems more relevant considering contemporary economic and social issues. The analysis of his contribution can be understood in the following ways:

Women education should be emphasized

First, policymakers in every country should place more emphasis on women’s education. Education is an essential condition for girls. Second, women should be able to enter the labour force after formal education. And there should also be no gender discrimination at the workplace, whether it is regarding the distribution of work or equal pay for equal work. There is also a gender gap in terms of salary and wages. It has historically been found in all regions. The wage gap between men and women has decreased over time, but the pace of decline has been slow. It also means that until there is a law for the welfare and safety of women in companies, jobs will continue to go to men.

This is the reality, and Goldin has also shown in her work that the gender gap does not necessarily disappear with economic growth, as large gaps exist in many economies. The first things that need to be changed in the interest of women are social norms, which especially act as a hindrance in a conservative society. Even after girls are fully educated, traditions may come in the way of getting a job. And it has been observed that as Western economies reached the developed stage, the proportion of women in the labour force increased, but this did not happen in developing countries in Asia and Africa.

What measures can governments take for this?

Along with increasing the attendance rate in school education, the government should also increase the enrollment of women in university education. Governments must start by prioritising gender equality and security. There is a need to provide a better environment for women. Factories should also compulsorily provide crèche facilities so that women do not have to leave work due to becoming mothers. ‘Work from home’ facilities can be extended to women employees to ensure that they can work long hours without leave. Often, even qualified women leave work and go home, then do not return, and sometimes even when they return under compulsion, their work changes.

Finally, many areas or tasks have been reserved for men for security reasons. This concerns low-paid services such as food delivery or public transport driving. Both areas are still the stronghold of men. Governments and policymakers should work to create an environment for women to work safely in a variety of roles and have financial independence.

The question is, will this help?

Maybe yes, this can be understood with some examples. For example, the Securities and Exchange Board of India (SEBI) has made it mandatory for companies to have at least one woman as a director on their boards. Similar steps can be considered for women in top management so that they can become role models for other working women.

The historic Women’s Reservation Bill recently introduced by the Government of India, which seeks to provide 33 percent reservation to women in the Lok Sabha and state legislatures, might be a crucial step in this direction. In many countries, the provision of women’s reservation has been given in the Constitution, or this provision has been made through a bill, whereas in many countries it has been implemented at the level of political parties only.

In Argentina (30 percent), in Afghanistan (27 percent), in Pakistan (30 percent), and in Bangladesh (10 percent), reservation has been provided to women by law, while the countries that have given reservation to women by political parties include Denmark (34 percent), Norway (38 percent), Sweden (40 percent), Finland (34 percent), Iceland (25 percent), etc.

Claudia Goldin’s winning the Nobel Prize in Economics is an opportunity for governments and policymakers around the world to be inspired to improve women’s participation in the labour market. This will not only help in diversity and gender empowerment but will also enable better utilisation of human resources.

(RFE/RL) — “Not all of this is the result of the work of our drones,” Ukrainian Navy spokesman Dmytro Pletenchuk said, but they have caused “quite a lot of damage to enemy ships.” (file photo)

The Russian fleet has suffered “serious damage” largely caused by Ukrainian drones, according to Ukrainian Navy spokesman Dmytro Pletenchuk, who said the tactics have made Ukraine the driver of a new type of naval warfare.

Pletenchuk, speaking on Ukrainian television on November 17, claimed that 15 Russian ships have been destroyed and 12 damaged since Russia launched its full-scale invasion of Ukraine.

“Not all of this is the result of the work of our drones,” he said, but they have caused “quite a lot of damage to enemy ships.”

Pletenchuk said this has made Ukraine a leader in “a new level of application of unmanned systems,” and is recognized as such.

“We have a separate team…that [uses] both surface and underwater drones. And not only for reconnaissance and demining, but also for destruction,” Pletenchuk said.

Russian forces in the Black Sea have recently “reduced significantly” thanks to the work of the Ukrainian defense forces, he claimed. He added that the Russian military has been forced to “remain as far away as possible and is significantly limited in its actions,” though the Ukrainian military previously has said that bad weather in autumn and winter typically forces Russian missile carriers to move into their base ports.

While the Russian position could be described as defensive, the enemy still has cruise missile carriers at its disposal, meaning the danger is still present, he noted.

Pletenchuk added that Ukrainian forces will continue their moves to weaken the Russian fleet.

“Of course, we will expand our influence at the first opportunity,” he said.

Russia has repeatedly claimed to have shot down drones over Crimea that appeared headed for its assets on the peninsula.

The Russian Defense Ministry said last week that a Ukrainian attack involving multiple drones on the Moscow-occupied Crimea region was repelled by Russian air defenses. A ministry statement said nine drones were destroyed and eight others were intercepted off the Black Sea coast of Crimea.

Ukrainian President Volodymyr Zelenskiy last month pledged to keep pressure on Russian-occupied Crimea after an attempted drone attack on the Moscow fleet installation in Sevastopol.

Zelenskiy said on October 24 that while Ukrainian forces have not yet gained full fire control over Crimea and surrounding waters, the “illusions” of Russia’s domination of Crimea “are melting.”

The thesis of Parag Khanna’s The Future is Asian is fairly obvious based on the title. Namely, Khanna predicts that Asian influence will come to dominate the 21st century, supplanting western influence. To support this conclusion, Khanna posits that, while the United States and Europe are distracted by internal political and economic turmoil, Asian powers will combine multilaterally and strengthen the region through international cooperation, potentially under the type of technocratic leadership that Khanna has built his career on advocating. Though many points are interesting and thought-provoking, Khanna’s arguments also contradict themselves at a number of key junctures.

Khanna appears primarily interested in soft power including cultural exports as well as large-scale economic phenomena involving trade. A number of chapters touch on topics such as global media as well as Khanna’s political preference for technocratic governments based on the Singaporean model. However, there are also plenty of arguments in this volume that should pique the interest of Security Studies enthusiasts, either as a point to critically contest or as a basis for further research. Some of these are regional – such as the notion that Asian powers will exert broader influence in Latin America and Africa. These are fairly viable proposals backed up by such real-world evidence as China’s increased investment in these regions, in an attempt to serve as an economic “gateway” for parts of Africa, as well as Asian states’ increased trade with Latin American countries. However, the main weakness of the text lies in the key points that constitute Khanna’s more general arguments.

These key points include a broad definition of Asia as “more of a sponge than a bloc”. Per Khanna’s definition, Asia is an expansive region that includes the Middle East and Central Asia – a portion of the continent that Khanna refers to broadly as “Southwest Asia. Additionally, one of Khanna’s more provocative arguments is that the west (including the United States) is distracted by its “China-centric” rhetoric, to the point of ignoring Asia’s multilateral rise as a region. However, Khanna’s notion of a multilateral Asian future also ignores the deep civilizational divides that exist within his expansive concept of Asia.

Khanna’s observations in The Future is Asian often prove themselves provocative at the expense of ending up deeply flawed. For example, Khanna appears unsure whether “Southwest Asia” is a part of the broad vision of a pan-Asian multilateralism he articulates, or whether the Middle East and Central Asian states he remarks upon constitute a network of client states for East Asian powers. In other words, Khanna’s view of the gulf states in relation to Asia more broadly paints them less as equal trading partners than a dependent periphery to China’s core. This in turn undermines his argument of a broad Asian multilateralism that includes the middle east (or, more broadly, Southwest Asia).

Additionally, Khanna’s view of China’s role in the Middle East seems to contradict his point that the United States is overly concerned about Chinese ambitions in Asia. Khanna, for example, points out that the Gulf States of the Middle East are increasingly looking toward China as a trade partner and moving away from the United States. Rather than proving Khanna’s point, this would imply that the United States is right to be concerned about competition from China, and that China-centric geopolitical rhetoric in the west is far from unfounded.

Moreover, Khanna’s main thesis – that Asia will gain power and influence through cooperation between its multifarious states – finds itself contradicted by Khanna’s own observations. Khanna notes, for example, that the idea of Asia is largely a social construct established by European powers to designate a cultural “other” to its east. Reaffirming this point, Asia constitutes a broad range of national identities that have little in common, making shaky ground for any future of cooperation.

Although Khanna makes an argument for his case that involves historical interconnectivity going back to the original Silk Road, this basis for his argument proves fairly weak in the face of well-defined intercultural and civilizational differences across Asia. Khanna’s most questionable statement throughout his book is one that reaffirms his main thesis: that Asia’s leaders anticipate a “humble yet productive commonwealth of commerce and learning”.

The Future is Asian is a provocative work that should be of interest to businesspeople, journalists, geographers, economists, and world travelers, but also – to a lesser extent – to scholars and practitioners of global security. Many of Khanna’s points, taken individually, would serve as a good devil’s advocate exercise for a course on geopolitical analysis or forecasting. However, although the work is interesting and worthy of academic discussion, many of Khanna’s more controversial arguments prove themselves self-contradictory, with a foundation built on sand rather than stone.